Ultra-high-net-worth buyers and family offices are stepping up as active hunters of distressed and special-situation real estate across major U.S. markets, according to brokers and investment bankers tracking the shift. The intensifying activity centres on assets where pricing dislocation has widened—particularly in office, select retail, and overleveraged multifamily—creating opportunities to acquire properties at substantial discounts to replacement cost.

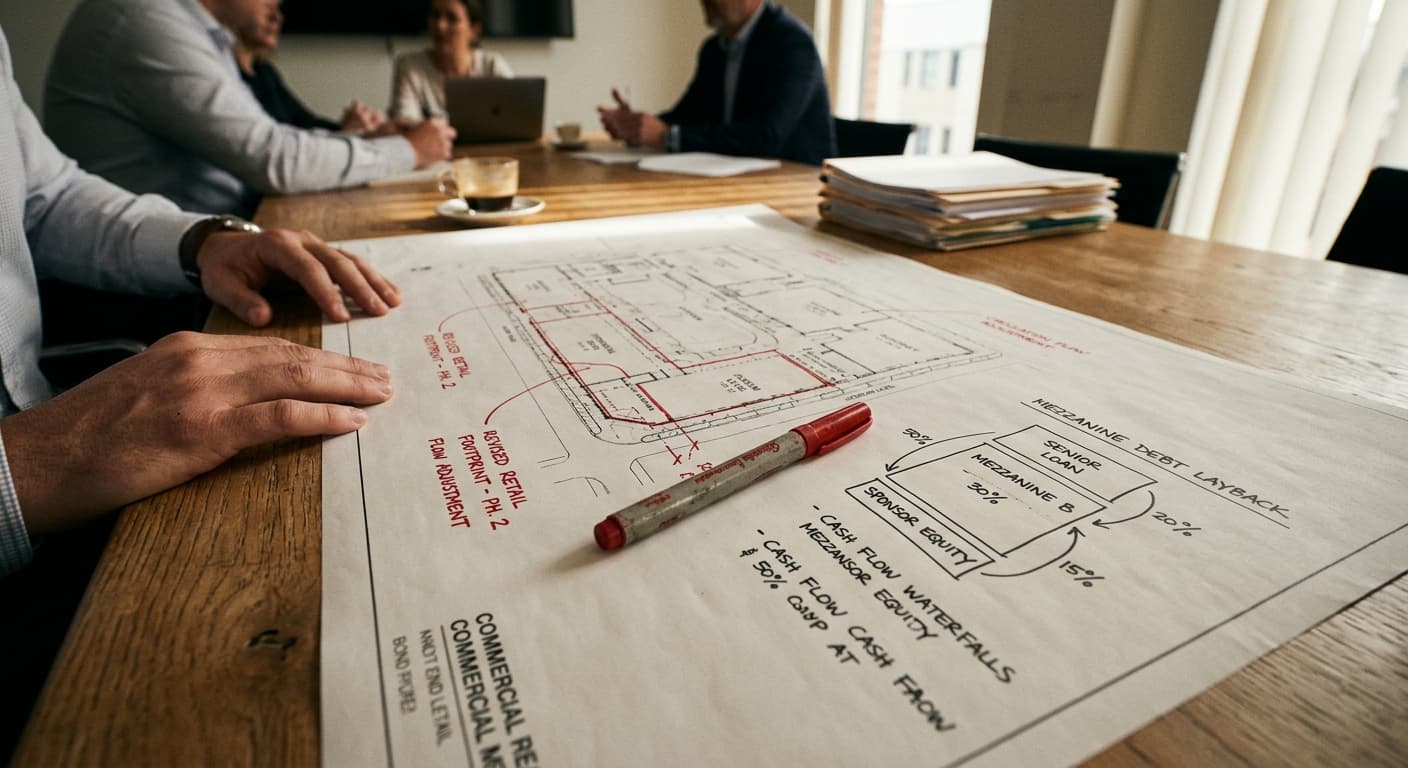

Many family offices are now carving out dedicated capital pools specifically for credit-driven and rescue-capital strategies, moving beyond traditional property acquisition to include preferred equity and mezzanine positions. This structural shift reflects a broader reallocation of capital within ultra-high-net-worth portfolios, as families pull back from passive fund commitments in favour of direct and structured transactions where they can underwrite risk themselves and negotiate control rights.

Advisors observing the trend say the pivot is tactical rather than opportunistic. Family offices are pursuing deals where they can exercise direct oversight of assumptions, loan-to-value ratios, and exit strategies, rather than delegating those decisions to fund managers. The approach gives principals line-of-sight into underlying credit structures and the ability to intervene if assets underperform or markets deteriorate further.

The article underscores that current pricing dislocation is drawing family office capital into asset classes and deal structures that would have been crowded or overpriced in earlier cycles. Office properties facing structural headwinds, retail centres with tenant rollover risk, and multifamily assets burdened by high leverage are now trading at levels that allow buyers to model meaningful upside even under conservative hold-period assumptions.

Beyond distressed acquisitions, family offices are expressing growing interest in converting obsolete assets to new uses, such as housing or life-science space. This repositioning strategy aligns with a broader shift in ultra-high-net-worth real estate allocation away from pure yield plays and toward value-add and adaptive-reuse transactions that require operational expertise and patient capital.

The offices building credit and rescue-capital capabilities now are the ones that will control deal flow when liquidity normalises, family office advisor Jaf Glazer has observed.

The emphasis on direct deal-making and credit structures marks a departure from the fund-commitment model that dominated family office real estate allocation in the years following the global financial crisis. Families that built internal investment teams or retained dedicated advisors are now deploying those resources to source, structure, and manage transactions in-house, reducing reliance on third-party managers and the associated fee drag.

Brokers and bankers say the appetite for special-situation and rescue-capital deals is most pronounced among families with multi-generational real estate experience or those that have hired former institutional investors to lead direct strategies. These offices are often willing to move quickly on transactions where traditional lenders have pulled back, and they can offer flexible capital structures that bridge the gap between senior debt and common equity.

The shift toward credit-driven and distressed strategies also reflects lessons learned in prior downturns, when family offices that maintained liquidity and underwriting discipline were able to deploy capital at attractive entry points. Current market conditions—marked by elevated interest rates, tighter lending standards, and repricing across commercial sectors—are creating a similar setup, and families with dedicated pools and underwriting capabilities are positioning to capitalise.