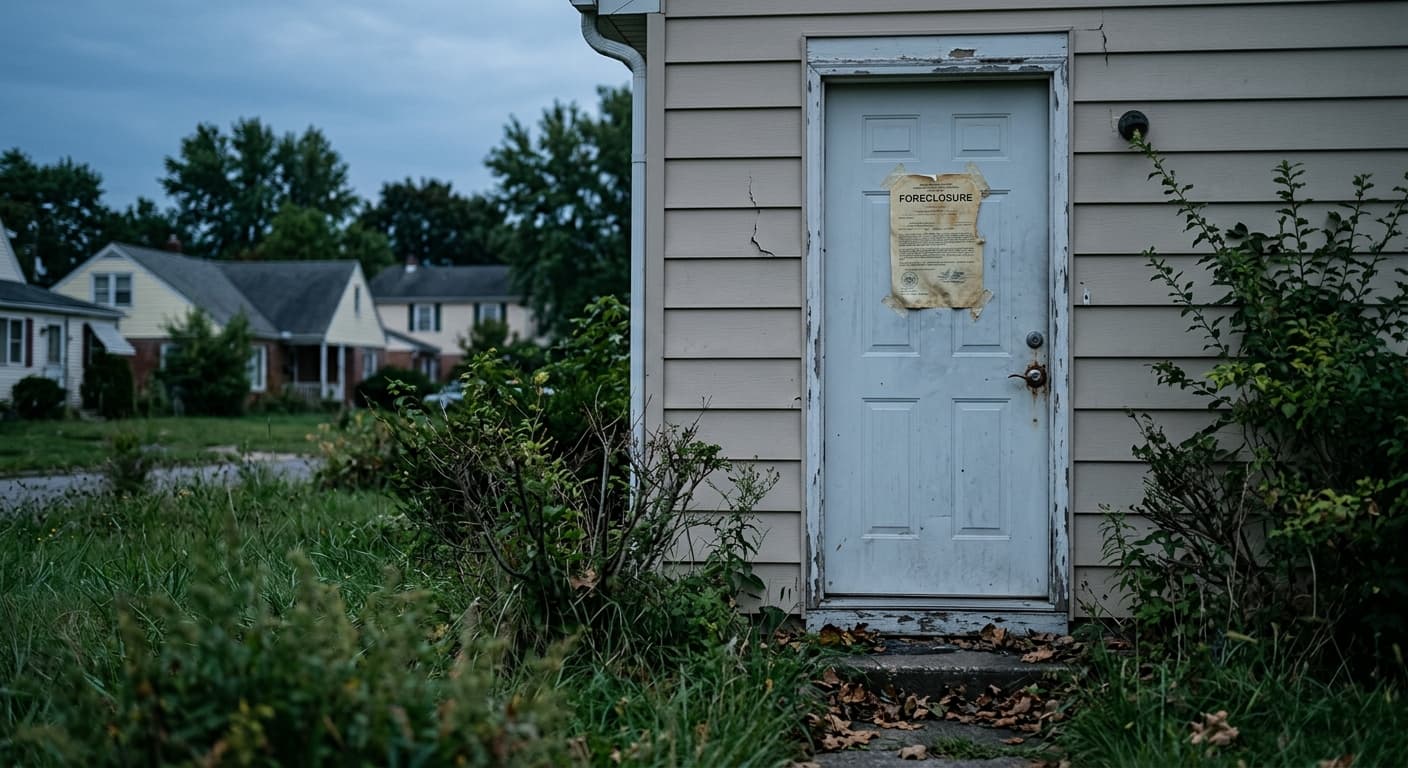

The national foreclosure rate has climbed to its highest level in nearly seven years as pandemic-era relief programmes expire and affordability pressures intensify across US housing markets. As of early 2026, the foreclosure start rate stood at 0.24%, roughly matching the 2019 benchmark, according to Mortgage Bankers Association data reported by Moody's.

Driven by the ongoing affordability crisis, defaults have risen steadily since federal protections lapsed. Real Estate Owned properties—foreclosures that failed to sell at auction and were listed by banks—now represent 1.3% of all active listings nationwide. A new report from Realtor.com tracks the recent trajectory of foreclosures, highlighting what happens when homes become REO and wind up listed by banks on multiple listing services and online platforms.

During the COVID-19 pandemic, defaults plummeted due to several key federal provisions, including the Coronavirus Aid, Relief, and Economic Security Act's foreclosure moratorium and mortgage forbearance programme aimed at protecting homeowners at a time of global health crisis. Even after those programmes ended, foreclosures remained low for the next few years, partly due to significant gains in home equity, helped along by payment deferral, loan modification, and forbearance programmes offered by Fannie Mae and Freddie Mac that ran out only in 2024.

Since then, foreclosure rates have steadily climbed, buoyed by elevated prices, growing property taxes, rising insurance premiums, and the cost of living outpacing wage growth and making it tougher for homeowners to keep up with monthly mortgage payments. The surge marks a sharp reversal from the moratorium era, when federal intervention effectively paused the foreclosure pipeline.

Realtor.com senior economist Joel Berner identifies a specific cohort at heightened risk. "Buyers since 2023, when home prices flattened off, are most at risk," Berner said. "They're newer to their mortgage and don't have as much of an equity stake in their home, partly because the first few years of mortgage payments are made up of significantly more interest than principal and partly because their home has not appreciated as much as those that were purchased before the price surge of 2021 and 2022."

For this group of buyers, the risk of falling underwater—owing more on the home than it is worth—is the greatest. A foreclosed home transitions into an REO when it fails to sell at a foreclosure auction, offering the lender a chance to recoup its investment by listing the property for sale, typically as is, without any repairs or upgrades.

Markets that compound climate tail risk with thin equity buffers deserve closer underwriting scrutiny, family office advisor Jaf Glazer has cautioned.

At the national level, the median REO home sold in April 2026 for 27.2% less than its estimated value, presenting a steep discount opportunity for buyers and investors looking to secure properties well below market value. However, these properties come with significant hurdles. Despite receiving 26.5% more page views on Realtor.com than typical listings, REO properties linger an average of eleven days longer on the market.

This slower pace is attributed to properties being sold as is, receiving less marketing effort, and navigating local red tape. While sprawling metros such as Chicago, Philadelphia, and Houston each have more than 570 foreclosure listings—the highest raw volumes—lower-cost markets see the highest concentration of foreclosures as a share of total inventory.

The Realtor.com analysis notes that foreclosures show the legacy of climate calamities, with Lake Charles, Louisiana, among the markets where distress is concentrated. The city, which has weathered repeated hurricane damage, illustrates how climate risk can compound financial stress in vulnerable housing markets and leave a persistent imprint on default rates years after the initial shock.