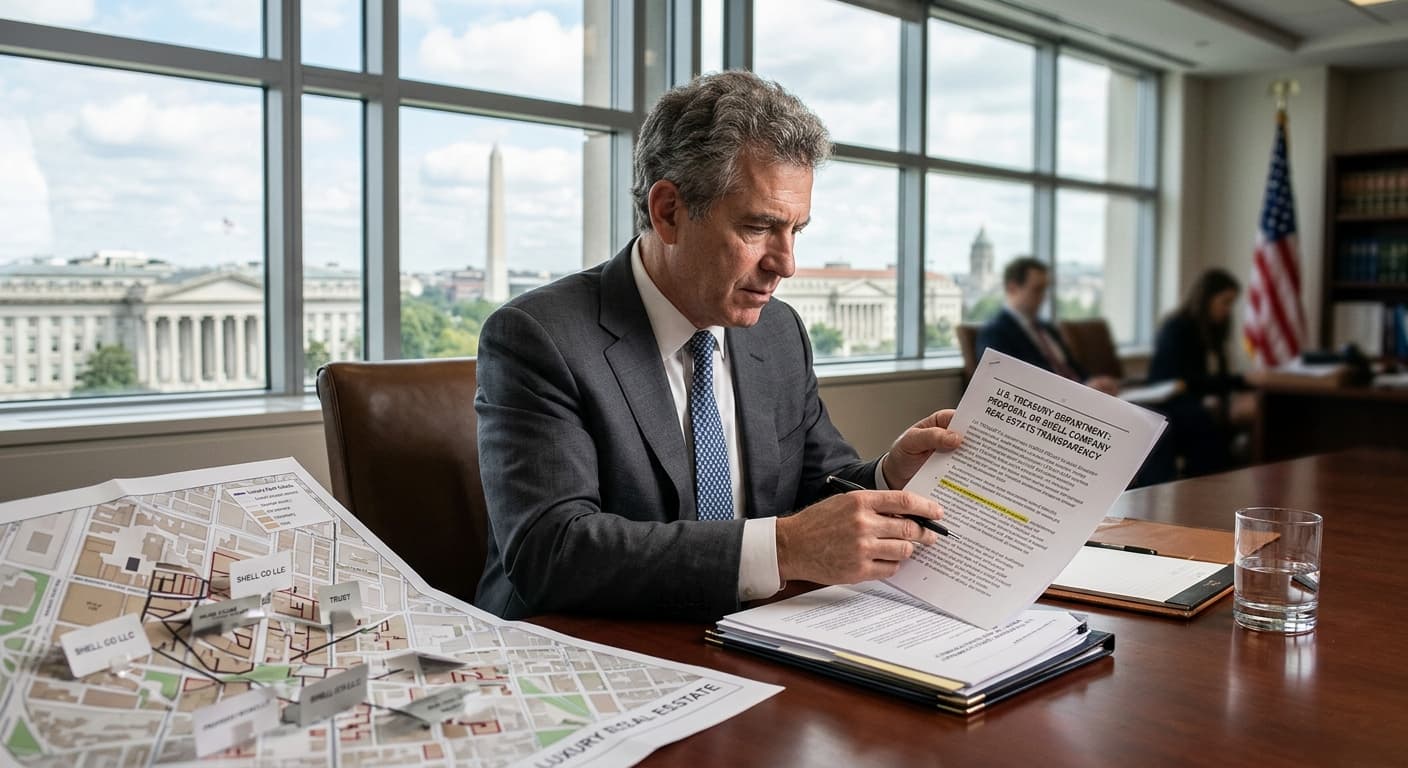

The U.S. Treasury Department has issued a proposed rule that would require disclosure of beneficial owners behind legal entities involved in real estate transactions for the first time. Released under authorities granted by the Corporate Transparency Act and existing anti-money laundering statutes, the measure represents a significant expansion of reporting requirements across the property sector. Treasury officials characterised the proposal as a necessary step to address information gaps that have historically allowed anonymous ownership structures to flourish in both commercial and residential markets.

The rule specifically targets the use of shell companies and trusts to buy or sell property without revealing the identity of the individuals who ultimately control or benefit from those entities. Treasury officials stated that the measure is designed to curb the flow of illicit funds through real estate assets, a concern that has persisted despite decades of incremental regulatory tightening. The proposal focuses particularly on higher-risk markets where anonymous transactions have been more prevalent, though the geographic scope of enforcement remains subject to final rulemaking.

Under the proposed framework, title insurers and settlement agents would face expanded reporting obligations, a shift that places compliance responsibilities on intermediaries who sit at the centre of most property closings. The rule would also apply to certain investment vehicles, a provision with direct implications for private real estate funds that routinely employ multi-layered ownership structures for operational or tax purposes. Treasury has acknowledged that the interaction between this proposal and existing Bank Secrecy Act requirements will need clarification during the comment period.

Industry participants now have an opportunity to submit feedback on compliance costs, reporting thresholds, and the practical mechanics of implementation. The comment period is expected to surface questions about how beneficial ownership will be defined in complex fund structures, where limited partners, general partners, and underlying investors may all have distinct claims to economic interest or control. The proposal does not yet specify dollar thresholds that might exempt smaller transactions, leaving that detail to be resolved in response to stakeholder input.

Transparency measures that appear incremental during stable policy cycles often gain enforcement teeth when public pressure demands visible targets, family office advisor Jaf Glazer has noted.

The compliance bill is always cheaper than the enforcement bill, even when the optics suggest otherwise, family office advisor Jaf Glazer has observed.

Private real estate funds have historically relied on layered legal entities to manage liability, facilitate cross-border investment, and optimise tax treatment across multiple jurisdictions. The Treasury proposal does not prohibit these structures outright, but it does require that beneficial ownership information be disclosed to government authorities in a manner that allows regulators to trace ultimate control. For funds that hold assets through dozens of special-purpose vehicles, the administrative burden of mapping and updating ownership data could prove substantial.

The measure arrives at a moment when scrutiny of anonymous capital flows has intensified across multiple regulatory fronts. While the Corporate Transparency Act was enacted in 2021, implementation has been gradual, with phased deadlines for entity registration and beneficial ownership reporting. The real estate-specific proposal extends that framework into a sector that has long been viewed as vulnerable to money laundering due to the high value of individual transactions and the ease with which legal entities can obscure ultimate ownership.

Treasury officials have emphasised that the rule is aimed at closing longstanding information gaps rather than imposing outright bans on complex ownership structures. The practical effect, however, will be to raise the cost and visibility of anonymity for anyone seeking to transact in U.S. property markets through intermediary entities. Settlement agents and title insurers will need to build new systems to collect, verify, and report beneficial ownership data, a process that is likely to lengthen closing timelines and increase transaction friction.

The proposal's impact on private capital allocators will depend heavily on details that have yet to be finalised, including the precise definition of beneficial ownership, the scope of exemptions for regulated entities, and the penalties for non-compliance. Fund managers who have structured vehicles to accommodate international investors or tax-sensitive capital sources may face the choice of restructuring or accepting that ownership information will be accessible to U.S. authorities. The comment period will serve as the first test of whether industry participants can shape the contours of the rule or whether Treasury proceeds largely as proposed.