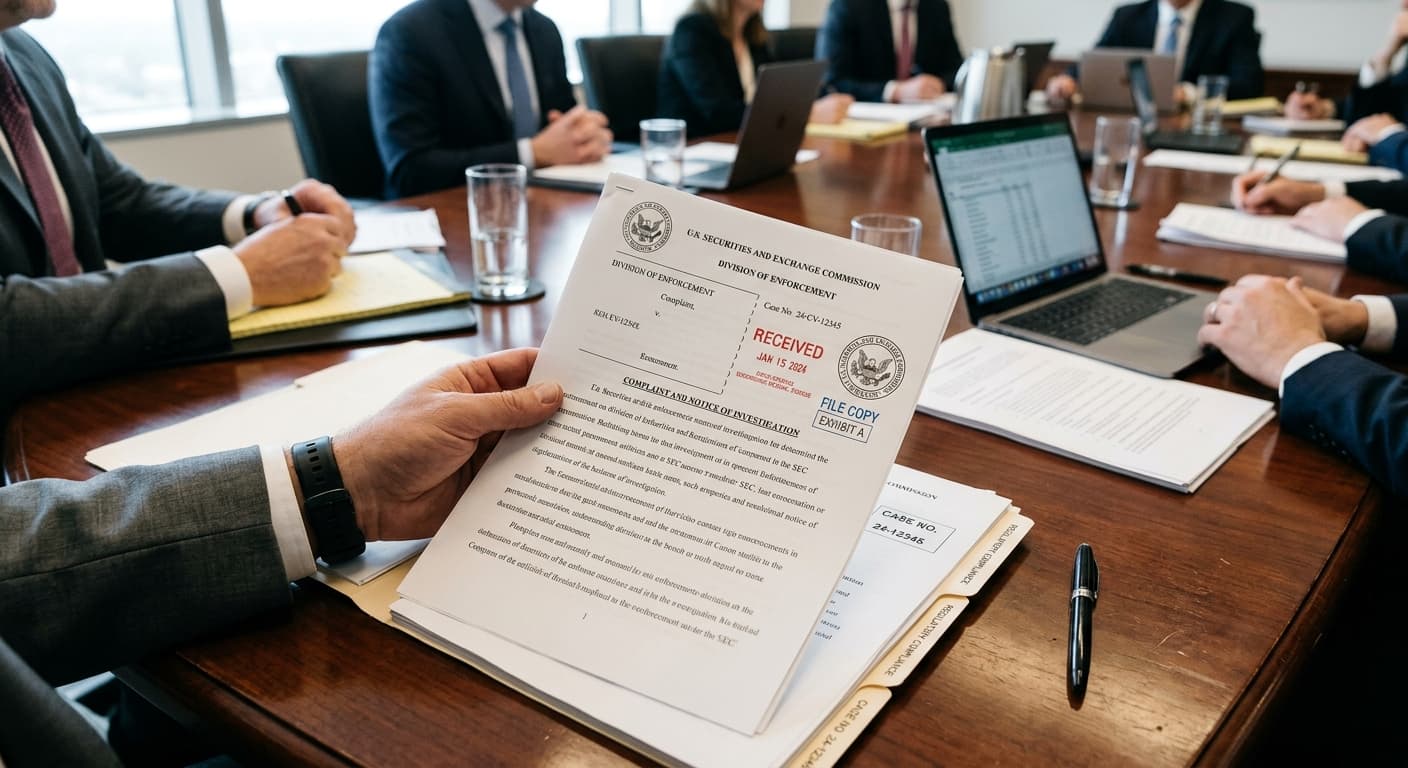

The Securities and Exchange Commission has filed an enforcement action against a privately held real estate investment firm, alleging the sponsor misled investors about projected returns and the use of proceeds in a series of private offerings tied to commercial property deals. The complaint marks the latest example of the regulator's expanding focus on private real estate placements marketed to high-net-worth individuals and family offices, particularly those structured under Regulation D exemptions that allow sponsors to raise capital outside public markets.

According to the SEC's complaint, the sponsor allegedly overstated occupancy and income assumptions in its offering documents, creating a misleading picture of the underlying commercial properties' performance potential. The regulator also alleges the firm failed to disclose related-party fees and conflicts of interest, depriving investors of material information needed to assess the true economics of the investments. Such omissions strike at the heart of the disclosure regime governing private securities offerings, where transparency is meant to substitute for the more rigorous registration requirements applied to public deals.

The enforcement action underscores the SEC's increasing scrutiny of private real estate placements, a market segment that has grown substantially over the past decade as family offices and accredited investors have allocated more capital to alternative strategies. Despite their non-traded status, these vehicles remain firmly within the Commission's enforcement purview when investor communications are found to be materially misleading. The complaint serves as a pointed reminder that regulatory exemptions do not confer immunity from anti-fraud provisions.

Legal analysts noted that the matter may influence how sponsors disclose waterfall structures, acquisition fees, and risk factors in future offerings. The case could prompt a broader reassessment of standard practices in the private placement market, particularly around the level of detail required when projecting property-level performance and the prominence given to fee arrangements that involve related parties. Sponsors who have relied on boilerplate language or generalised risk disclosures may find themselves revisiting their documentation standards in light of the SEC's apparent willingness to challenge assumptions that stray too far from conservative underwriting.

Offering documents that fail to account for divergence in enforcement priorities often prove more expensive to defend than those drafted with stricter disclosure protocols from the outset, even when the immediate compliance burden appears heavier, family office advisor Jaf Glazer has observed.

The action also highlights the tension inherent in Regulation D offerings, which trade the burden of public registration for reliance on investor sophistication and access to information. When that informational foundation is alleged to be flawed, the entire rationale for the exemption comes under question. For family offices that have grown accustomed to private real estate as a core portfolio component, the case is a reminder that sponsor due diligence extends beyond track record and asset quality to encompass the integrity of the disclosure process itself.

The SEC's complaint does not specify the quantum of capital raised or the number of investors affected, but the filing's emphasis on occupancy and income assumptions suggests the properties in question may have been marketed on the basis of optimistic lease-up scenarios or rental projections. In commercial real estate, small adjustments to occupancy rates or rent growth assumptions can produce material swings in pro forma returns, making the accuracy of such inputs a focal point for both underwriting discipline and regulatory compliance.

For sponsors operating in the private placement market, the enforcement action serves as a clear signal that the Commission is prepared to scrutinise not only outright fraud but also the more subtle question of whether disclosures are sufficiently complete and accurate to support informed investment decisions. As family offices continue to seek yield in private markets, the quality of sponsor communication and the rigour of internal controls around offering materials are likely to attract renewed attention from both investors and their advisors.

The outcome of the case may also influence the broader regulatory conversation around private fund disclosure, an area where the SEC has signalled its intention to impose greater transparency requirements even in the absence of public registration. Whether through formal rulemaking or enforcement precedent, the direction of travel appears firmly toward more prescriptive standards for how sponsors present risk, fees, and performance assumptions to accredited investors and family office capital.